My Experience Presenting at IEEE CAI 2026: Large Language Models for Stock Price Forecasting

- Olivia Zhang

- May 17

- 3 min read

During May 8 - 10, I attended the IEEE Conference on Artificial Intelligence, where I presented two of my research papers. One of them, “A Review of Large Language Models for Stock Price Forecasting from a Hedge-Fund Perspective,” explores how large language models (LLMs) can be applied to stock price forecasting from a practical investment perspective. This work, coauthored with Dr. Zhang, summarizes my research throughout 2025, during which I worked as a portfolio management intern at Lumos Alpha, a hedge fund that applies artificial intelligence to investment management.

The presentation day was truly exciting. Many attendees joined the session and listened carefully to my talk. I believe many were curious about an important question: What is the gap between academic researchers, who focus on algorithmic innovation, and hedge fund practitioners, who focus on generating real investment returns using algorithms? This was exactly the perspective I hoped to share in my presentation.

My paper consists of three main parts.

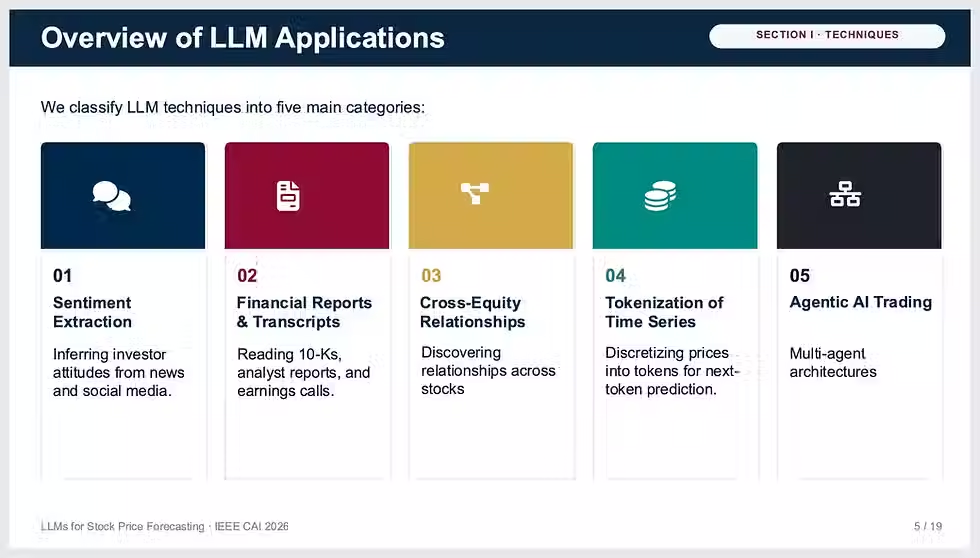

The first part provides an overview of LLM applications in stock price forecasting. While many review papers discuss the broad applications of LLMs in finance, they often cover too wide a scope. My work narrows the focus to a specific niche: the use of LLMs for stock price prediction. Based on literature published from 2022 to early 2025, I categorize these LLM applications into five major areas: sentiment extraction for predicting market movements, analysis of financial reports and earnings call transcripts, identification of cross-equity relationships, tokenization of stock price data for next-token prediction, and the use of agentic AI systems.

The second part of my work, which I consider the most important, discusses key challenges in applying LLMs to stock forecasting. These include issues such as sentiment analysis reliability, data leakage, database limitations, performance evaluation, illiquidity, and market predictability. In reviewing many academic papers, I found that some of these concerns are often overlooked or insufficiently addressed. For example, many studies evaluate model performance over very short time horizons, sometimes only a few weeks or months. From a hedge fund perspective, this is far from sufficient. At Lumos Alpha, a trading algorithm must be tested across multiple market environments, including both bull and bear market cycles, alongside other rigorous evaluation strategies. Strong performance over a short period alone says very little about an algorithm’s long-term robustness.

Finally, I concluded the presentation by sharing several suggestions for future research directions and practical improvements in applying LLMs to stock price forecasting.

I was especially glad to see that many attendees took photos of my presentation during the session. It was encouraging to know that the audience found the material valuable, and I hope my work will be helpful to others researching this topic.

Following the presentation, we had a Q&A session. Because many attendees were highly interested in the topic, the discussion lasted longer than usual. Even after the session ended, several professors and industry professionals approached me with additional questions. We had engaging and insightful conversations about the challenges and opportunities in stock price forecasting.

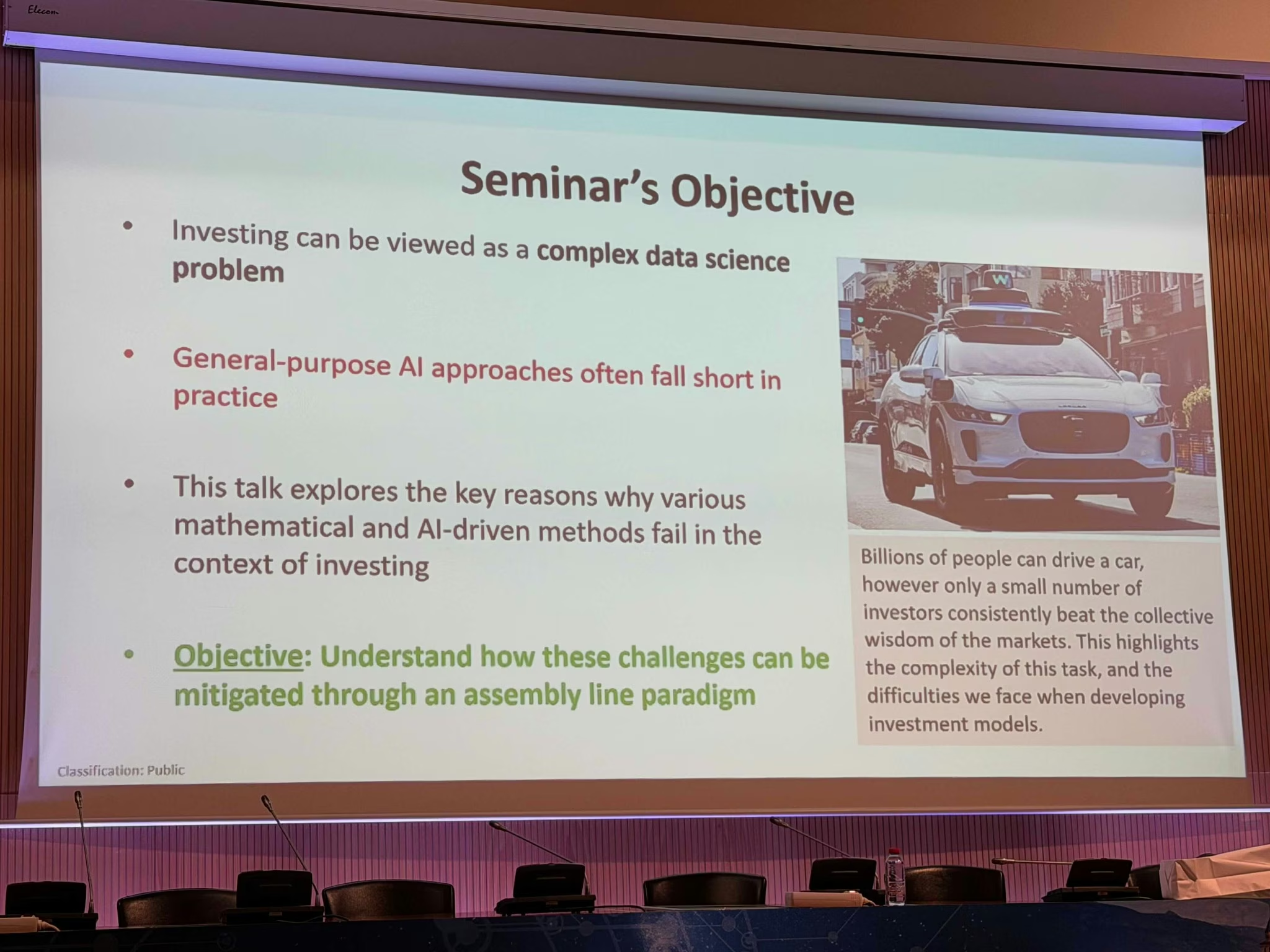

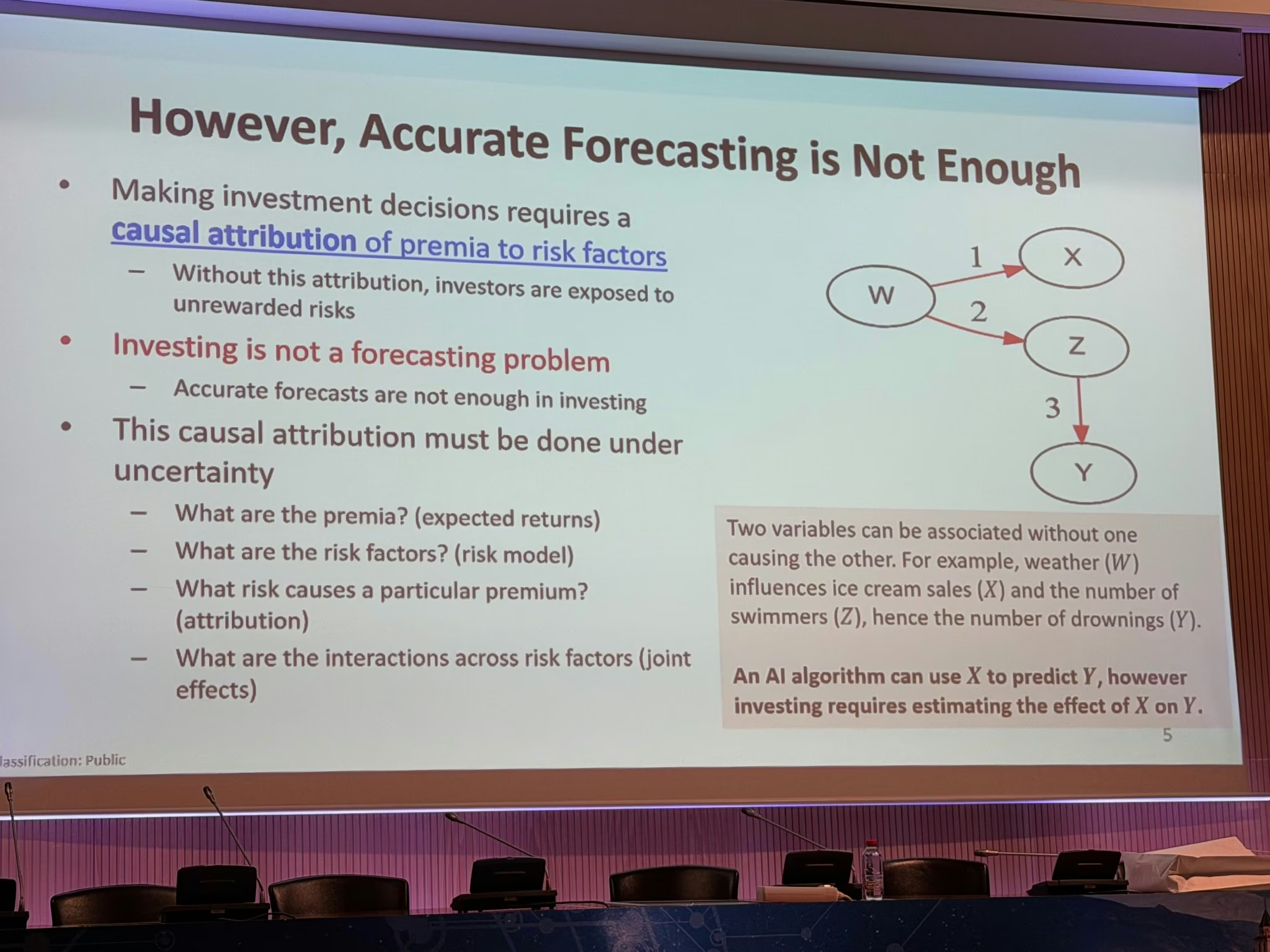

That day would not have been complete without attending the keynote speech by Marcos López de Prado. Professor López de Prado is a highly respected and influential researcher in financial machine learning and quantitative finance. His keynote, titled “AI Challenges in Mathematical Investing,” emphasized an important idea: while correlations between factors, equities, or assets are often unstable and unreliable, identifying true causal relationships is crucial for successful investing. Yet this is particularly difficult in practice because most AI algorithms excel at detecting statistical correlations rather than genuine causal mechanisms.

I strongly resonated with this perspective. In financial markets, there are countless situations in which equities or assets appear highly correlated during some time, yet no real causal relationship exists. As a result, these correlations may disappear unexpectedly over time. This was also one of the key issues I discussed in my presentation.

Coincidentally, I had recently started reading Professor López de Prado’s well-known book, Advances in Financial Machine Learning. After the keynote, I had the opportunity to ask for his signature and take a photo with him. It was a very memorable moment!

Read your paper. Really nice work, very informative! Keep going!